Some of the links on this page are affiliate links. When you make a purchase through an affiliate link, I earn a commission at no cost to you. See my entire disclosure policy for all the boring details.

Where is all my money going?

How much should I budget in this category?

I want to save money but I never have any leftover…

It seems like emergencies come up a lot…

If you’ve had any of those thoughts, you are not alone. Maybe you’ve made a budget, but it still feels like it’s not really working. In order to stick to a budget, you have to have some method how to track your spending. Hopefully, today’s post will help you answer some of those above dilemmas.

(If you don’t yet have a budget in place, start here: How To Start a Budget. Then come back when you’re done reading that.)

If you make a plan for your money, you want to know you’re sticking to the plan, right? If you plan to spend $400 on food per month, the only way to know if you’re sticking to your $400 budget, is tracking your spending at grocery stores. Over the past 5 years, we have tried a lot of different methods for tracking spending (including the method of not really tracking spending at all…)

Perhaps this we-learned-the-hard-and-long-way post will save you some time and guessing.

For simplicity sake, let’s use this easy sample budget. Pretend you make $1000 per month. You are going to spend the following:

$300 rent

$300 groceries + household items

$20 fun

$20 gym membership

$20 kids stuff

$20 life insurance

$20 phone bill

$50 transportation costs

$250 debt pay-down

Obviously a lot of those numbers are unrealistic, but they’re easy to work with for today’s lesson.

Some expenses you have are fixed – rent, gym membership, life insurance, phone bill, debt minimums. Those numbers aren’t changing. You can plug those into your budget pretty easily and track them pretty easily because they’re usually paid once a month. We have most of our bills set to auto pay from our bank account halfway through the month (except rent is on the first of the month). Also, I pay our internet bill manually since internet companies like to scam people and I don’t trust them on auto draft with all their mysterious fee & bill increases. (Something I learned the hard way – ahem – Century Link.) But I won’t go into that right now. 🙂

It is not hard to figure out your fixed expenses or track them.

Tracking the variable expenses, such as groceries, fun money, and transportation costs, gets a little trickier. The reason it’s harder to track variable expenses is because you often spend out of these categories multiple times per month. While understanding that budgeting and managing money takes some time, energy, and diligence, you also don’t want to spend hours upon hours trying to figure out where that $20.00 went and how much you really spent at the grocery store. Therefore, a relatively easy-to-manage system for how to track spending is the goal.

Everyone processes things differently, and there are a lot of different money-tracking systems that work. It’s not a matter of right and wrong. The goal is to track spending in a way that makes sense to you so you can stick to your budget.

Oh, the other goal is not to lose your mind in the process. It took us 5 years to figure out what works for us. So, if it takes you a few months to figure out what works for you (and your spouse, if you have one of those), you’re ahead of the game. No big deal! Stick with it!

In the spirit of you not having as hard a time with this as we did, here’s a bonus tip: if you wait until the end of the month to enter all your transactions, tracking will be miserable. I speak from experience. Sitting down by yourself or with a spouse once a month and looking at all your spending for the month is a surefire way to hate budgeting forever.

Honestly, I now like to track expenses as often as possible. Once a week is our preference. If we wait more than 10 days, I’m usually kicking myself, the “money date” is less fun, and we’re both crabby.

So, don’t wait. Track your spending frequently. Especially when you’re new to budgeting. It’ll be much easier!

Here are a 3 suggestions for simple & specific methods THAT ACTUALLY WORK for tracking spending.

1. App/ Software/ Online Tool

There are tons of budgeting apps, software programs, and online tools to help you manage your budget and track your spending. The 3 major online or software budgeting tools I am most familiar with are YNAB, Mint.com & EveryDollar. I know there are tons of other apps out there – if you have one to recommend, feel free to leave it as a suggestion in the comments.

We have tried all 3 and currently use YNAB. In my opinion, it is the best budgeting tool on the planet. I highly highly recommend it!!! (I used to recommend EveryDollar, but this post explains why we like YNAB better.)

YNAB (You Need A Budget)

- free 34 day trial (no credit card info required to start)

- $50 annually or $5/month after that – WELL WORTH IT, in my opinion.

- web based, meaning you go to ynab.com to access your budget, or you can use the app.

- the budget is 100% customizable

- you can enter transactions manually and/or connect to your bank accounts, credit cards, etc.

- automatically does “roll-overs” for categories from month to month which makes budgeting for christmas gifts or that once-a-year insurance payment easy peasy lemon squeezy as my 1st graders used to say.

- encourages you to save up one month’s expenses ahead of time so that you are no longer living paycheck to paycheck

- app available

- There are free classes and tools on YNAB’s website to help you get started with managing money and they’re good!

- been around for a while, so it’s very polished & user friendly.

- free; you use it online

- connects to all accounts for free (banks, credit cards, student loan payments, etc…)

- you create a budget

- they automatically categorize all your spending.

- you manually have to correct the incorrect categorizations, but over time the program gets better at learning your spending habits and you need fewer and fewer manual “fixes” as you use it longer

- iPhone & Android app available

- see my complete review here

- free, online

- create your own budget & manually enter transactions

- option to pay $99 per year if you want to connect to your bank account to see the transactions in your budget. (We used to do this. it’s was and a huge time saver). Similar to YNAB in this way. The transactions don’t get automatically categorized for you; you have to click and drag them to the correct category. Clicking and dragging feels like spending money.

- you can choose whether or not $ rolls over by turning that category into a “fund.”

- iphone app available; android app coming soon

If you go digital for budgeting, choose a program that makes sense to you. One reason Ben and I both like YNAB is because it visually makes sense with how we both think about money. It visually matches how we organize our information mentally. Also, we use our debit cards (as credit) for most purchases, so we love the ease of YNAB having all our transactions right there for us to track. We prefer to track them manually (as opposed to having mint automatically categorize them) because it ‘feels’ more like spending money to us. Plus, nothing can slip through the cracks. We have to pay attention and put every dollar somewhere in our budget.

There are tons of users on all 3 of those, so they’re all doing something right! Poke around the different sites and tutorials and see which one makes sense to you.

2. Cash

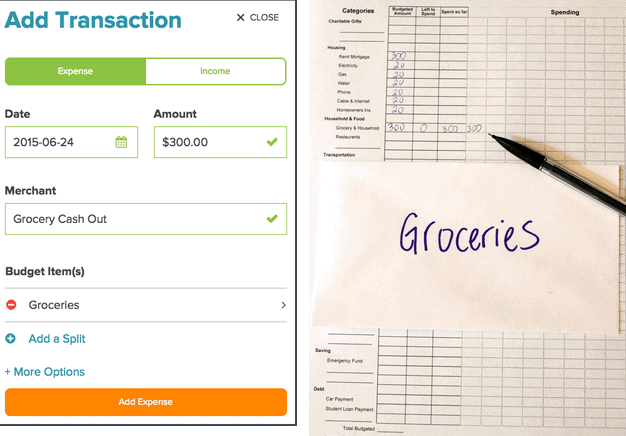

When you use cash for a budget category, you only have 1 transaction to track – the initial cash withdrawal. For example, say you wanted to use cash for groceries + household from our above sample budget. There is $300/ month allotted for groceries. So, at the beginning of the month, go get $300 from the bank. Track that one expense in your budget spreadsheet or app.

[minus 300] And you’re done, for the month. Win!!

Put that cash in an envelope titled “Groceries & Household.” Whenever you buy food, use that cash. Do not use that cash for anything else. Do not buy food with any other money or with your credit card. When the cash is gone, no more food. So spend carefully 🙂 As you spend money out of that cash envelope, there’s no need to really track it in your budget throughout the month, because you already tracked the initial withdrawal at the beginning of the month.

We used to use cash for everything. I wrote more details about how to do a simple cash envelope system here. Currently, the only categories I take cash out for are groceries and my personal spending money. We each get a little spending money every month. I take mine out in cash at the beginning of each month and put it in my wallet. If I want to save it up for something more expensive, I put it in an envelope in a drawer in our house so I don’t have it on me to spend on starbucks. We use debit cards (run as credit, from the same checking account) for everything else.

For cash to work, you have to develop the mental and emotional discipline to NOT SPEND WHEN THE CASH IS GONE. If you didn’t bring the cash with you, don’t buy anything. No card substitutions.

Honestly, cash keeps things simpler. If you HATE the idea of tracking spending, but you want to be on a budget, maybe cash is for you. It’s a little bit of up front hassle, but it is no hassle throughout the month.

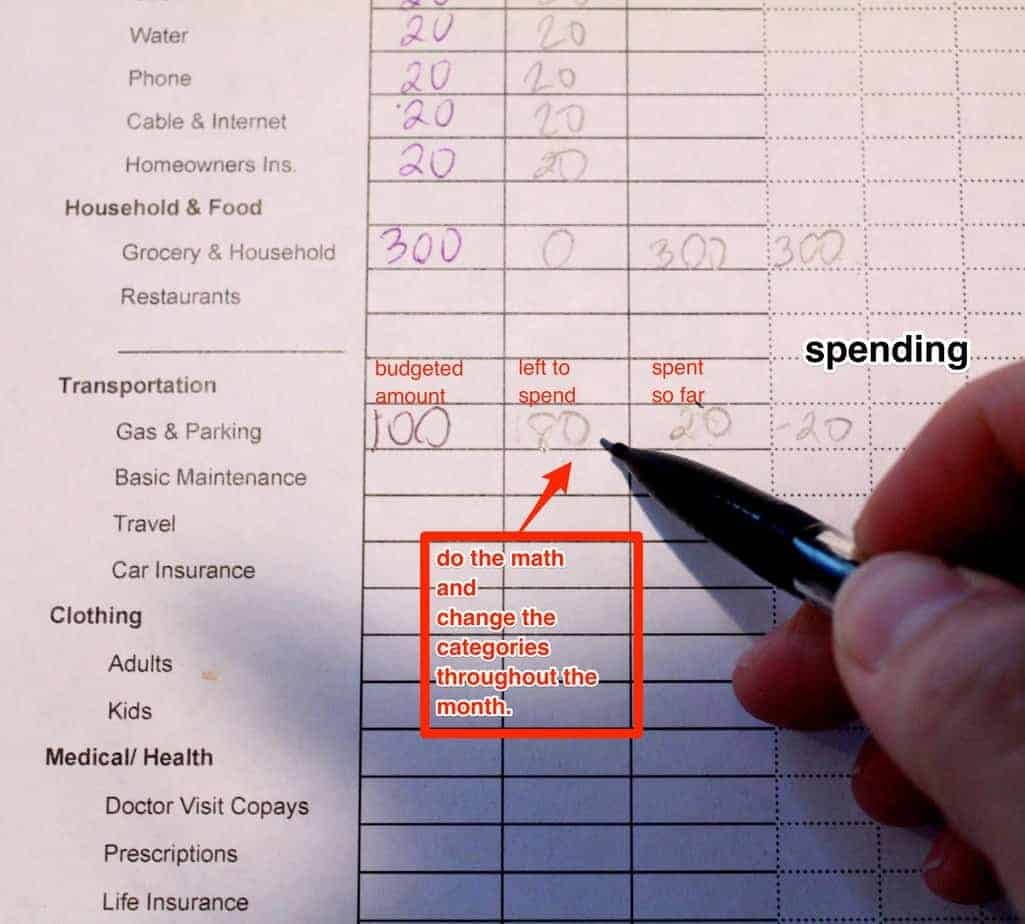

3. Pencil & Paper

Say you’re not a cash-carrying kinda guy (or gal). You could print this blank budgeting spreadsheet out each month, and keep it on your fridge. [Here is a budgeting spreadsheet that has category suggestions. There are also lots of other resources for online templates, or you can make your own. Another one I really like is in this post.]

Whenever you spend money, fill in the spreadsheet as soon as you get home. Write the amount spent in the appropriate category and manually change the amount you have remaining in that category.

If you’re like me, and always need to do 17 things for your kids who seem to think they’re lives are falling apart when you walk in the door, another option would be to keep a little basket somewhere safe + easily accessible, near your spreadsheet. Throw your receipts in there and then write all the numbers on the spreadsheet at the end of the day or a couple days a week.

If you use this method, it requires organization with 3 things:

- Saying “YES” when the person asks if you want your receipt

- Putting that receipt somewhere where it’s not going to get lost on your way home.

- Remembering to enter the receipts several times a week.

I am WAY too flaky for all that so this didn’t work very well for us. A hybrid version of this is using a digital spreadsheet.

3b. Digital Pen & Paper (aka: Spreadsheet)

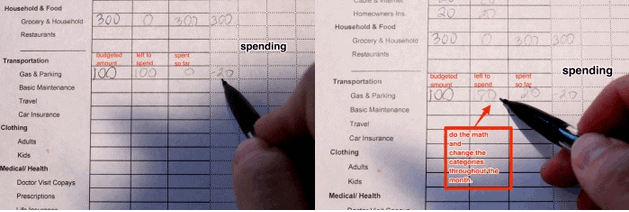

You could do the same thing as I mentioned above, but digitally on a spreadsheet. We used a spreadsheet for a LONG time. Our spreadsheet had all the formulas plugged in, so as we entered our spending to the right, the numbers in the “left to spend” column changed. Here is the free spreadsheet download – you can click file–> make a copy to get your own editable copy. Each week, we’d pull up our bank account online. We’d go through every purchase from that week and enter it in the spreadsheet. We had a lot of our spreadsheet automated, but it was still pretty tedious. Also, you have to be careful not to miss transactions with this method.

Conclusions

I think the biggest components of finding a system that works for you are:

- Choosing what fits your personality and way of thinking. Spreadsheets aren’t for everyone. Neither are apps. Find what works for you!

- Sticking with it, begin diligent, knowing spending-tracking will pay off in the long run. I wrote more about how to actually stick to your budget here.

By tracking your spending you will figure out where your money is going, how much you are realistically spending on various items, and if there’s any haphazard spending you can cut in order to reach your financial goals!

So, do you track spending? How?

Happy Budgeting 🙂

-Renee

This post is #2 in my Budgeting 101 Series. You can find the rest of the posts here.

Thank you! That makes sense 🙂

Hi Karolina, so glad this is helping you, thanks for reading! It took us a while to figure out scenarios like that too. What I would do in that situation is – just keep the leftover cash from, for example January, in your envelope. Then take out February’s money and add to it. If you’re consistently coming in under budget,then you can adjust your grocery budget down a little. I’ve found that ours ebbs and flows a little because of things like laundry detergent, cleaning supplies, or a meat sale or baking ingredients… So one month I end up with an extra $20 but then the following month, several bigger supplies might run out and I’ll need the extra $20. Does that make sense? Hope it helps!

Hi I just started reading your blog and have found it so helpful 🙂 thank you! I can’t seem to wrap my brain around this though, it should be simple… I want to combine the cash and debit card use into my budgeting. My question is- when I withdraw the money for my monthly grocery budget (I’ll use groceries as an example) I like the idea of just withdrawing once and not having to add in the spent cash as I go for that category but if I have money left over for the month do u add it to next months grocery budget? But how do I account for it if I’m not making the adjustments for money used.. It would seem like money not allocated… Anywhoo any insight into this would be greatly appreciated! Thank you!!